Current Trends in Mortgage Interest Rates in Canada

Introduction

Mortgage interest rates play a crucial role in the Canadian housing market, influencing both buyers and lenders. As of late 2023, the landscape of mortgage interest rates has seen significant fluctuations, primarily due to the Bank of Canada’s monetary policies aimed at curbing inflation. Understanding these trends is imperative for prospective homeowners and investors alike, as they impact housing affordability and market dynamics.

Current Rates and Trends

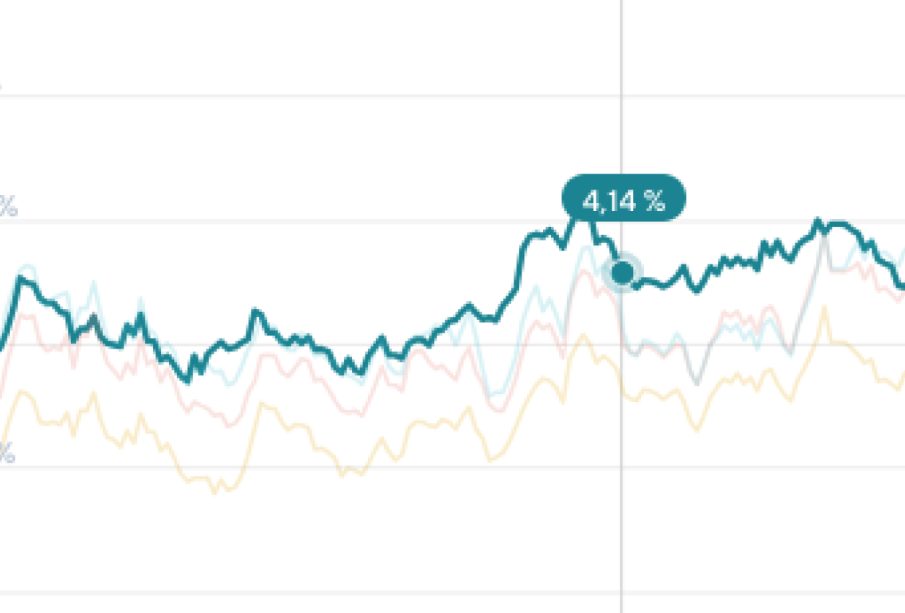

As of October 2023, mortgage interest rates in Canada have experienced a steady increase over the past year. The Bank of Canada raised its benchmark rate multiple times in an effort to combat persistently high inflation, resulting in average fixed mortgage rates reaching as high as 6.5%, while variable rates hover around 5.4%. Recent reports indicate that the increase in borrowing costs has led to a slowdown in home sales, particularly in major markets like Toronto and Vancouver.

Impact on Homebuyers

The rise in mortgage interest rates has notably affected potential homebuyers. First-time homebuyers face particularly challenging conditions, as higher rates mean increased monthly payments. According to the Canadian Real Estate Association (CREA), the average price of homes has decreased somewhat due to reduced demand; however, the stark jump in borrowing costs often negates any price decline. This situation has prompted many buyers to re-evaluate their purchasing power and consider alternative options such as renting or waiting for more favorable market conditions.

Future Outlook

Looking ahead, experts predict that mortgage interest rates may stabilize in 2024. Analysts suggest that if inflation continues to ease, the Bank of Canada might consider holding rates steady or even lowering them. However, uncertainties tied to global economic conditions and domestic inflation trends complicate predictions. Homebuyers and investors are advised to stay informed about upcoming economic reports and central bank meetings that may influence future rate decisions.

Conclusion

The current state of mortgage interest rates in Canada underscores the complex nature of the housing market. As interest rates rise, their effects ripple through the economy, impacting affordability and demand. For both current homeowners and prospective buyers, staying informed about these trends will be essential in navigating the market and making sound financial decisions. Understanding the implications of rising rates can help Canadians prepare for future opportunities, whether they pertain to homeownership, investments, or financial planning.